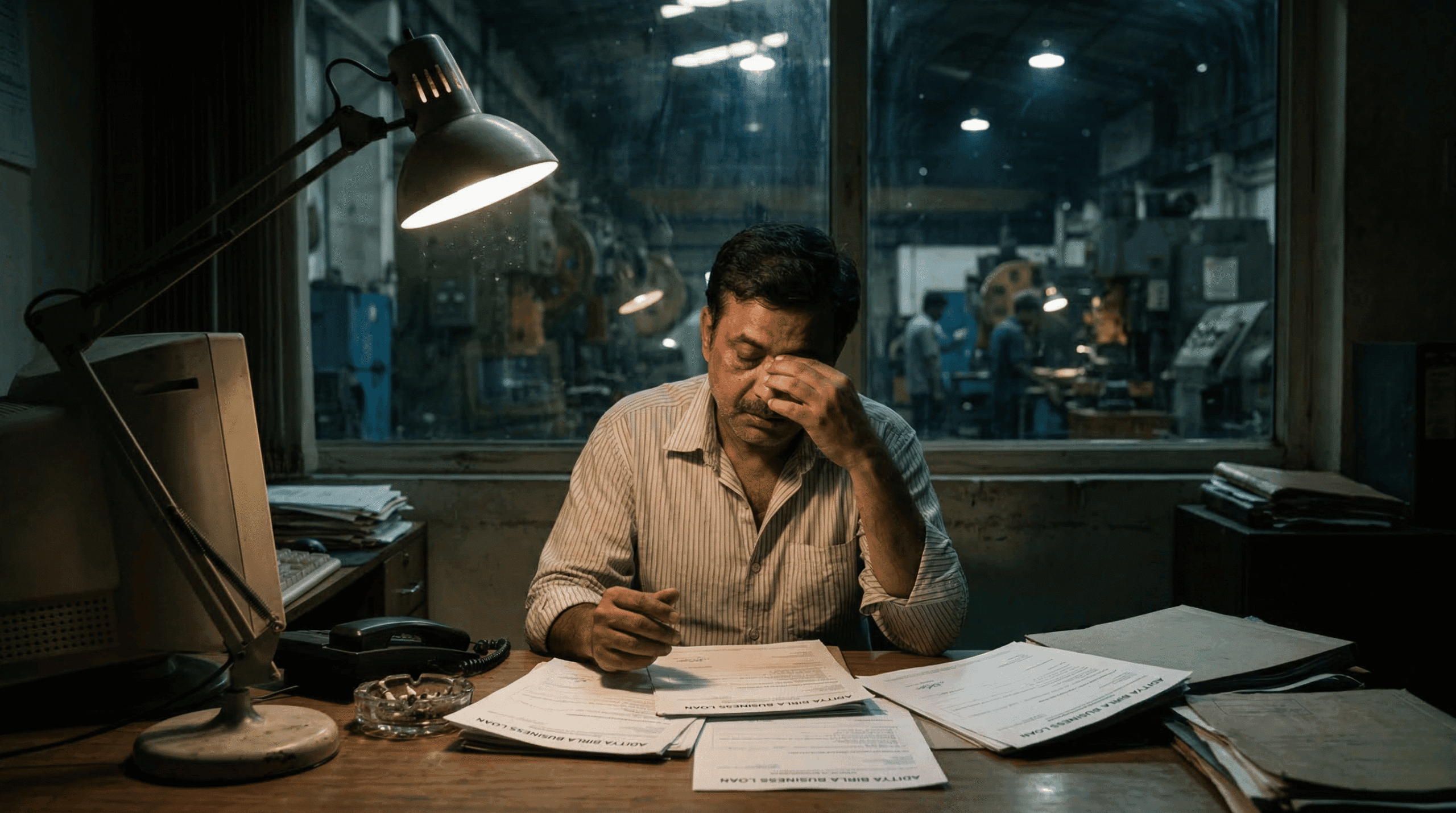

The metallic clatter of dead machinery is a haunting sound. It was a blistering Tuesday afternoon in Surat, and my factory floor was eerily quiet. Dust motes danced in the harsh sunlight filtering through the grimy clerestory windows. Total silence.

My bank account was actively bleeding cash. I had exactly fourteen days to pay my yarn suppliers, or they would permanently cut off my credit line. Panic, hot and sharp, clawed at my throat.

Applying for an aditya birla business loan felt like shoving my entire financial history through an industrial woodchipper. Every past mistake, every delayed vendor payment, suddenly became a glaring red flag. I assumed my three years of steady manufacturing revenue would guarantee a quick cash injection.

I was completely, utterly wrong. A brutal awakening.

And this is exactly where most desperate entrepreneurs bleed out. You walk into the application process blind, assuming a decent credit score is a golden ticket. The underwriters sitting in their air-conditioned Mumbai offices do not care about your dreams or your late-night hustle.

They care about cold, unforgiving math.

The Brutal Truth About Securing an Aditya Birla Business Loan

The initial rejection email hit my inbox like an unexploded ordinance. I stared at the screen, my heart hammering against my ribs. The relationship manager cited a minor discrepancy in my Form 26AS.

It was a tiny tax mismatch from two years prior. Just a clerical error by a junior accountant. But to the algorithmic gatekeepers assessing my aditya birla business loan, it signaled absolute chaos.

Why? Because institutional lenders operate on a baseline of severe paranoia. They scrutinize your gross profit margins with forensic intensity.

I needed fifty lakh rupees to acquire two imported Tsudakoma ZAX9100 air jet looms. Without those machines, my production capacity would remain stagnant, and my competitors in the Sachin GIDC industrial estate would swallow my market share whole.

So, I decided to aggressively reverse-engineer their entire approval matrix. I spent seventy-two waking hours dissecting every line of my financial audits. I dragged my accountant back into the office on a Sunday morning.

We ripped apart three years of balance sheets. Nothing was left unexamined.

Cracking the Aditya Birla Business Loan Underwriting Matrix

You must understand the distinct dividing line between unsecured and secured capital. Unsecured financing is a highly volatile gamble for any non-banking financial company. They are handing you up to fifty lakh rupees without a single piece of collateral holding you down.

Naturally, the barrier to entry is vicious. You need a CIBIL score north of 675 just to get a seat at the table. A score of 674? Automatic system rejection.

But a good credit score is merely the entry fee. The true battleground is your business vintage. You must prove, unequivocally, that your enterprise has survived the grueling reality of the open market for at least thirty-six months.

I had to pull my audited profit and loss statements, my Udyam Registration certificate, and twelve agonizing months of GST returns. They want to see a consistent, unbroken chain of cash flow. A single bounced cheque in your bank statement will derail the entire process.

7 Best Tax Saving Mutual Funds: Insane Wealth Builders – PayApprove

I learned quickly that Aditya Birla Capital heavily scrutinizes your Debt Service Coverage Ratio (DSCR). If your existing obligations consume too much of your monthly revenue, they will immediately classify you as a high-risk flight hazard.

I had to aggressively pay down a toxic high-interest overdraft facility just to make my balance sheet look palatable. It felt like draining my own blood to buy a bandage.

The Udyog Plus Digital Labyrinth

The days of walking into a mahogany-paneled bank branch with a leather briefcase full of paper are dead. I navigated their entirely digital Udyog Plus platform. The interface is deceptively simple, hiding a fiercely complex backend verification system.

You input your PAN card, and the system instantly pulls your entire financial ghost. It knows about that delayed credit card payment from forty months ago. It knows about your fluctuating tax liabilities.

And you cannot hide behind creative accounting.

I uploaded my documents, my hands physically shaking over the keyboard. The system demanded my latest utility bills, my firm’s Memorandum of Association, and my personal KYC documents.

Every single file had to align perfectly. If the address on your GST certificate deviates by a single comma from your lease agreement, the system flags you for manual review. Manual review is a polite term for a bureaucratic purgatory that can swallow your application for weeks.

To survive this, you must audit your own paperwork before the algorithm does. Check the official MSME portals to ensure your Udyam registration exactly mirrors your current operational data. Consistency is your only weapon here.

The Cost of Capital: Interest Rates and Hidden Bloodletting

Let us talk about the actual price of this money. The marketing brochures prominently advertise rates starting from 14 percent. That is a highly sanitized fiction meant for pristine, massive corporations.

As a mid-sized textile manufacturer battling supply chain issues, my offered rate was significantly higher. The unsecured term loan bracket routinely stretches up to 21 percent depending on your specific risk profile.

I sat in my cramped office, punching numbers into a battered desktop calculator. The Equated Monthly Installment (EMI) on a thirty-six-month term loan was staggering.

You must factor in the processing fees, which easily chew up 2 to 3 percent of the sanctioned amount upfront. Before a single rupee even hits your operational account, the lender has already extracted their flesh.

But I had no alternative. The Tsudakoma looms were sitting in a customs warehouse, racking up daily demurrage charges.

The Secured Alternative for an Aditya Birla Business Loan

When the unsecured route looked too expensive, I briefly considered leveraging my physical property. The secured aditya birla business loan ceiling is massive, stretching up to twenty-five crore rupees.

They will finance up to 95 percent of a residential property’s value. But industrial plots? The Loan-to-Value (LTV) ratio violently drops to 75 percent.

I owned the factory shed in Surat, but pledging the physical roof over my machinery felt terrifying. If the textile market collapsed—a notoriously common occurrence—the lender would legally seize my entire livelihood under the SARFAESI Act.

I read through the Reserve Bank of India’s Fair Practice Code just to understand my theoretical rights during a recovery scenario. The legal jargon was dense, cold, and highly intimidating.

I ultimately refused to pledge the factory. I chose the aggressive, unsecured path. I would rather pay a brutal interest rate than risk losing the concrete beneath my feet.

The Anatomy of a Working Capital Demand Loan

Not every financial crisis requires a massive term loan. Sometimes, you just need oxygen to survive a temporary suffocating gap in cash flow.

I discovered the Working Capital Demand Loan (WCDL) buried deep in their product roster. This is a drastically different beast compared to a standard term loan.

You are not borrowing a lump sum for heavy machinery. You are securing a revolving line of credit strictly to keep the lights on. Paying daily wages. Buying raw polyester yarn.

Interest is calculated solely on the exact amount you draw down, not the total sanctioned limit. This specific mechanism actually saved me thousands of rupees during the slow monsoon season when my buyers routinely delayed their invoice payments.

I used the supply chain financing option to discount my pending receivables. Basically, I sold my unpaid invoices to the lender for immediate cash, minus a steep discount rate. It hurts your net profit, undoubtedly.

But liquidity is survival. Profit is just a theory on a spreadsheet if you cannot meet your weekly payroll.

The Interrogation and the Final Verdict

On the eighth day, my phone vibrated. An underwriter was on the line, demanding a verbal explanation for a sudden dip in revenue during the previous October.

My mouth went completely dry.

I explained the reality of the Diwali production slump. The factory shuts down, migrant workers return to their villages, and billing completely halts for three weeks. I sent him historical industry data to back up my claim.

He remained utterly silent on the other end of the line. Just the faint hum of static.

“We need updated bank statements for the last forty-eight hours,” he finally commanded.

I scrambled. I pulled the data, digitally signed the PDFs, and uploaded them within twenty minutes. The sheer physical exhaustion of the process was breaking my spirit. I was spending more time appeasing algorithms than actually running my manufacturing floor.

You must be prepared to defend every single financial decision you have made over the last thousand days. They will question your vendor choices. They will question your inventory holding costs.

Do not flinch. Do not apologize. Present your business logic with aggressive clarity.

The Weight of the Sanction Letter

The approval notification finally flashed on my screen on a humid Thursday evening. The requested fifty lakh rupees, sanctioned at a rigid 17.5 percent interest rate.

I printed the sanction letter. The paper felt unusually heavy in my hands.

The money hit my current account seventy-two hours later. The digital zeroes looked incredibly surreal on my banking dashboard. I immediately wired the funds to the customs agent to release the Japanese looms.

I didn’t celebrate. I didn’t open an expensive bottle of whiskey. I just sat alone in the dark, dusty factory, listening to the ambient noise of the industrial estate outside.

I had successfully navigated the labyrinth. I had the capital. But the real bloodbath—scaling the factory to actually service that massive new debt—was just about to begin.

Are you actually prepared for the terrifying reality of suddenly getting the money you begged for?